We offer a Safe Pair of Hands for clients in vulnerable circumstances

Code of Professional Standards

All individual Members and Associate firms of the Consumer Duty Alliance shall, always:

Act in good faith in all dealings with clients

Always avoid causing foreseeable harm to clients

Inform, empower and support clients to pursue their financial needs, objectives and aspirations

Fully disclose, clearly explain and consciously mitigate any conflicts of interest identified in our dealings with clients, including where commercial interests might conflict with a client's best interests

Only offer products or services that are both suitable and needed, offering fair value and transparent pricing

Ensure clients receive the support they need, when they need it

Embrace a focus on customer vulnerability including adherence to the Consumer Charter of the Financial Vulnerability Taskforce

Inform, empower and support clients to pursue their financial needs, objectives and aspirations.

Kymin Financial Services Ltd -

Our Vulnerable Client Policy

This policy sets out how Kymin Financial Services Ltd aims to identify and treat clients and prospective clients who may be considered as being vulnerable whether by their age, a disability or circumstances.

Although vulnerability can come in many forms, it is important that such individuals are always dealt with appropriately, fairly and in a consistent manner.

Definition of a

vulnerable client

The Financial Conduct Authority defines a vulnerable client as: “Someone who, due to their personal circumstances, is especially susceptible to harm, particularly when a firm is not acting with appropriate levels of care”

All clients are at risk of becoming vulnerable, whatever their age or financial status, on a permanent, temporary or sporadic basis. This risk is increased by characteristics, related to four key drivers of vulnerability:

-

severe or long-term illness, physical disability, hearing or visual impairment, mental health condition or disability, addiction and low mental capacity or cognitive disability.

-

retirement, bereavement, income loss, divorce, domestic abuse, financial abuse and new caring responsibilities.

-

low ability to withstand financial or emotional strain i.e. inadequate or sporadic income, too much debt, low savings.

-

lack of knowledge or confidence in managing finances, poor literacy or numeracy skills, poor English language skills, poor or non-existent digital skills, learning difficulties and poor access to help and support.

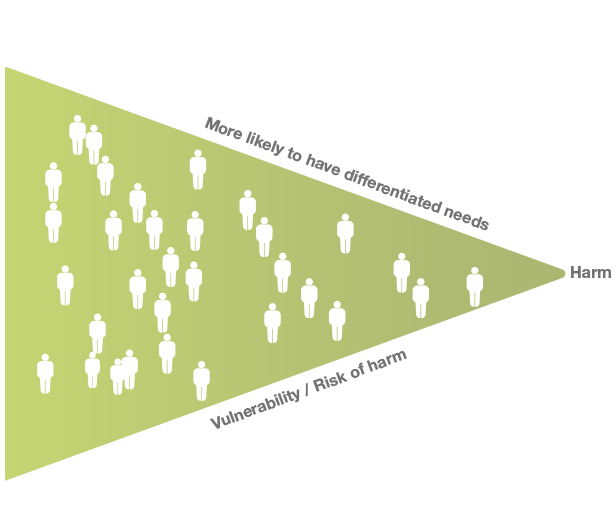

The vulnerability spectrum

The Financial Conduct Authority (FCA) have adopted the concept of a “spectrum of vulnerability”. Clients can move up and down this spectrum depending on their circumstances. Being vulnerable is transient and not a fixed state.

Customers to the left of the spectrum are less likely to be vulnerable than those to the right, who are deemed at greatest risk of harm. The Consumer Duty regulations state that where people in vulnerable circumstances are at greater risk of harm, firms should take additional care to ensure they achieve outcomes as good as those experienced by consumers deemed not vulnerable.

Where a firm can identify a customer in vulnerable circumstances, and support them effectively, the risk of harm is reduced. The FCA require more consistency among firms so that consumers get a more equal service whichever firm they interact with.

Put simply the Consumer Duty raises the standard of care afforded to all consumers. Their financial guidance sets out what firms should do to ensure that clients in vulnerable circumstances experience outcomes at least as good as those for other clients.

To quote the FCA directly “Consumer in vulnerable circumstances may have additional needs to be at greater risk of harm if things go wrong. For this reason, the Duty, makes explicit reference to firms paying attention to the needs of customers with characteristics of vulnerability”

The principles of good consumer outcomes need to be embedded into the culture, policy and procedures of a firm. A firm’s vulnerable customer policy for example should not just be a tick-box exercise, but one that is re-visited often and at every touch point of the customer’s journey. It should come naturally to all employees to focus on good customer outcomes for ALL clients, wherever they sit on the vulnerability spectrum.

The vulnerability spectrum

The Financial Conduct Authority (FCA) have adopted the concept of a “spectrum of vulnerability”. Clients can move up and down this spectrum depending on their circumstances. Being vulnerable is transient and not a fixed state.

Customers to the left of the spectrum are less likely to be vulnerable than those to the right, who are deemed at greatest risk of harm. The Consumer Duty regulations state that where people in vulnerable circumstances are at greater risk of harm, firms should take additional care to ensure they achieve outcomes as good as those experienced by consumers deemed not vulnerable.

Where a firm can identify a customer in vulnerable circumstances, and support them effectively, the risk of harm is reduced. The FCA require more consistency among firms so that consumers get a more equal service whichever firm they interact with.

Put simply the Consumer Duty raises the standard of care afforded to all consumers. Their financial guidance sets out what firms should do to ensure that clients in vulnerable circumstances experience outcomes at least as good as those for other clients.

To quote the FCA directly “Consumer in vulnerable circumstances may have additional needs to be at greater risk of harm if things go wrong. For this reason, the Duty, makes explicit reference to firms paying attention to the needs of customers with characteristics of vulnerability”

The principles of good consumer outcomes need to be embedded into the culture, policy and procedures of a firm. A firm’s vulnerable customer policy for example should not just be a tick-box exercise, but one that is re-visited often and at every touch point of the customer’s journey. It should come naturally to all employees to focus on good customer outcomes for ALL clients, wherever they sit on the vulnerability spectrum.

Identifying a vulnerable client

The presence of one or more of the types of vulnerability does not necessarily mean that a client is deemed to be vulnerable. We will continue our personal approach and our relationship with the client when we assess each individual client’s personal circumstances and ensure that every client is treated with respect, care and empathy.

In all cases the Kymin Financial Services Ltd team will ensure the following:

seek consent to obtain, record and retain sensitive personal data

robust records are created and retained

obtain copies of anti-money laundering verification from the client and if necessary, from attorneys or deputies

“We can assess each individual client’s personal circumstances and ensure that every client is treated with respect, care and empathy.”

Robin Hall, Managing Director

Dealing with vulnerable clients

We will always make sure that a client has the capacity to understand the advice that they are being given.

If we identify a client as being vulnerable or becoming vulnerable, we will consider the following:

Vulnerability - All types

Where clients are identified as being vulnerable the client file will be clearly marked to enable speedy identification

Clients will be encouraged to invite a family member or trusted third party to participate in future meetings

Should any of the team at Kymin Financial Services Ltd have any concerns that the client is being pressured into a particular course of action by a family member, the advice process will be postponed until the client can be met on their own

Where appropriate the client will be offered meeting times outside of standard office hours

The client will be offered a choice in how we communicate with them

Where appropriate, the client will be given the option to have a further meeting to give them the opportunity to discuss any recommendations or arrange for a third party to attend

Vulnerability - physical disabilities

Clients will be given the option (where appropriate) for Kymin Financial Services Ltd adviser to attend their premises or a location of their choosing

Information can be provided in large print if requested and where available from providers

Hearing difficulties – Clients will be offered the opportunity to invite a sign language interpreter of their choosing.

Vulnerability - where English is not the client's first language

Clients will be offered the opportunity to invite an interpreter of their choosing to all meetings at their cost

Vulnerability - not being computer literate

Clients who have indicated difficulty using computers and/or electronic communication platforms will have correspondence sent by post.

To discuss any of the points mentioned above please contact us today.

Start a new relationship with your finances.

Don’t let any more time pass you by. Contact us today to discover how we can help you to achieve the life you have always dreamed of and make it become reality.